If you have ever carefully listed out your itemized tax deductions before, especially if you own a home, consider a different approach now. With the updated standard tax deduction amount for your specific filing status, you might find it more advantageous to take the standard deduction instead of itemizing your tax deductions.

The latest data from the IRS reveals that approximately 90% of individuals filing taxes are now opting for the standard deduction, a shift largely attributed to changes implemented through the Tax Reform legislation in 2017. If you find yourself uncertain about the most advantageous choice for this tax year, consider utilizing our convenient tax deduction calculator or reaching out to our specialized tax experts for personalized guidance throughout the entire process.

In just a short amount of time, grasp the modifications in the standard deduction and itemized deductions, and receive an approximate calculation of your deductions depending on the information provided. Additionally, this tool advises you on whether to opt for standard or itemized deductions and offers suggestions on year-end tax strategies to enhance your itemized deductions.

In general, when your standard deduction outweighs your itemized deductions, opting for the standard deduction is usually the more advantageous choice.

Should I take the standard vs. itemized tax deduction

Contemplating whether to opt for the standard deduction or dive into the itemized deduction realm? The decision of which one will yield a greater tax benefit for you is contingent upon your specific situation. Let’s delve into different scenarios where either the standard or itemized deduction would be most advantageous.

When you should take the standard deduction

Understanding the complexities of tax preparation may appear overwhelming at first, yet rest assured, assistance is within reach. The choice between opting for the standard deduction or itemizing largely hinges on your eligibility for various deductions. The standard deduction represents a fixed sum determined by your tax filing status, offering supplementary advantages for individuals aged 65 and above or with visual impairments.

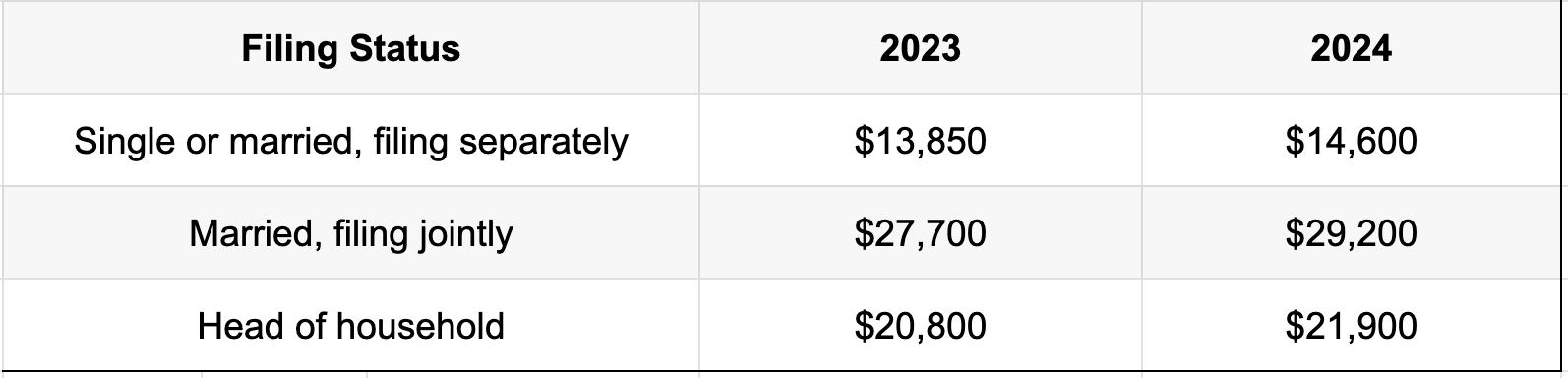

The current standard tax deduction is:

- $13,850 for single filers

- $13,850 for married, filing separately

- $20,800 for heads of households

- $27,700 for married, filing jointly

Each year, the IRS updates the standard deduction figures to account for inflation. As a result, it is important for you to review your expenditures annually in order to determine the best strategy for your situation if you have itemized deductions such as mortgage interest and property taxes.

In the upcoming tax year of 2023, significant inflation adjustments have been implemented, marking one of the largest increases in decades at 7.1%. This adjustment may lead to the standard deduction surpassing your itemized deductions for the year, making it more advantageous to opt for the standard deduction.

In plain terms, choosing the standard deduction is the best decision when the total of eligible itemized expenses falls short of the standard deduction threshold. When contemplating whether to go with the standard deduction, it is crucial to evaluate itemized deductions like mortgage interest, medical costs, and charitable contributions to inform your tax-filing decision-making process.

When you should take the itemized deduction

Wondering about the right time to consider itemizing deductions? It becomes beneficial when your qualifying expenditures, such as medical expenses, mortgage interest, or donations to charity, exceed the standard deduction threshold. By itemizing deductions, you could potentially reduce your tax liability if these eligible expenses surpass the standard deduction amount.

In certain scenarios, it is possible for taxpayers to find themselves in a situation where their itemized deductions match the standard deduction amounts set at $13,850 for single filers and $27,700 for married couples filing jointly. To overcome this, individuals could consider strategies such as increasing their charitable donations towards the end of the tax year or ensuring they include all eligible charitable contributions when filing their taxes, thereby elevating their total itemized deductions above the standard deduction threshold.

Exploring potential qualifying expenses can be made easier by consulting our article on often-overlooked deductions. Utilize our calculator that compares standard and itemized deductions for a clearer picture. Additionally, our team of dedicated tax professionals at PriorTax will tailor their guidance to your specific circumstances without requiring you to distinguish between standard and itemized deductions.